Types of DSO Buyers and How Each Prices Your Practice Differently

Cluster Edition

- Published

- May 17, 2026

- Edition

- PPR-CLUSTER-D3-2026-V1

- Publisher

- Private Practice Research

- Plain text mirror

- /types-of-dso-buyers.txt

Suggested citation

Private Practice Research. (2026). Types of DSO Buyers and How Each Prices Your Practice Differently (Report No. PPR-CLUSTER-D3-2026-V1). Private Practice Research. https://privatepracticeresearch.org/reports/types-of-dso-buyers

Edition: PPR-CLUSTER-D3-2026-V1 Status: Published Prepared by: Private Practice Research Editorial Staff. Methodology Desk. Published: 2026-05-17 Last Updated: 2026-05-17

PPR Research Note This cluster page is part of the Transitions Research Program. Every numerical claim is footnoted to a named institutional or trade source. This article does not represent a valuation, does not constitute legal or tax advice, and is not affiliated with any dental transition broker or DSO. Authorship: Private Practice Research editorial staff.

Part of: The Complete Dental Practice Transition Decision Framework · Cluster: DSO Dynamics

Executive Summary#

Four DSO buyer archetypes (Platform DSO, Portfolio DSO, DPO, MSO) price practice acquisitions through materially different cash mixes, rollover-equity terms, employment commitments, and post-close autonomy structures. This cluster page presents the PPR DSO Buyer Archetype Matrix with offer comparisons on a $1.2M practice showing how archetype choice affects total realized proceeds over a six-year transition window.

What are the four types of DSO buyers?#

The four types of DSO buyers fall into structurally distinct archetypes: Platform DSOs (greenfield-builders acquiring practices to launch new regional brands), Portfolio DSOs (PE-backed acquirers folding established practices into existing brands), DPOs (Dental Partnership Organizations distributing equity among contributing dentists), and MSOs (Management Service Organizations providing administrative support without practice ownership).

Each archetype offers materially different cash mixes, rollover-equity terms, employment commitments, post-close clinical autonomy, and capital-stack exposures. Sellers who understand the archetype that approaches them can predict offer terms before they arrive and prepare counter-offers accordingly.

The DSO acquisition market in 2026 includes approximately 250 to 350 active DSO and DPO entities in the United States per ADA News and AGD Impact reporting. The count has grown from approximately 100 to 150 in 2018 as private equity sponsors have funded multiple new platforms. Platform DSOs and portfolio DSOs together account for approximately 80 percent of DSO acquisition activity by dollar volume. DPOs and MSOs account for the remaining 20 percent but are growing as practitioner-equity-retaining structures gain traction with sellers who want continued clinical autonomy.

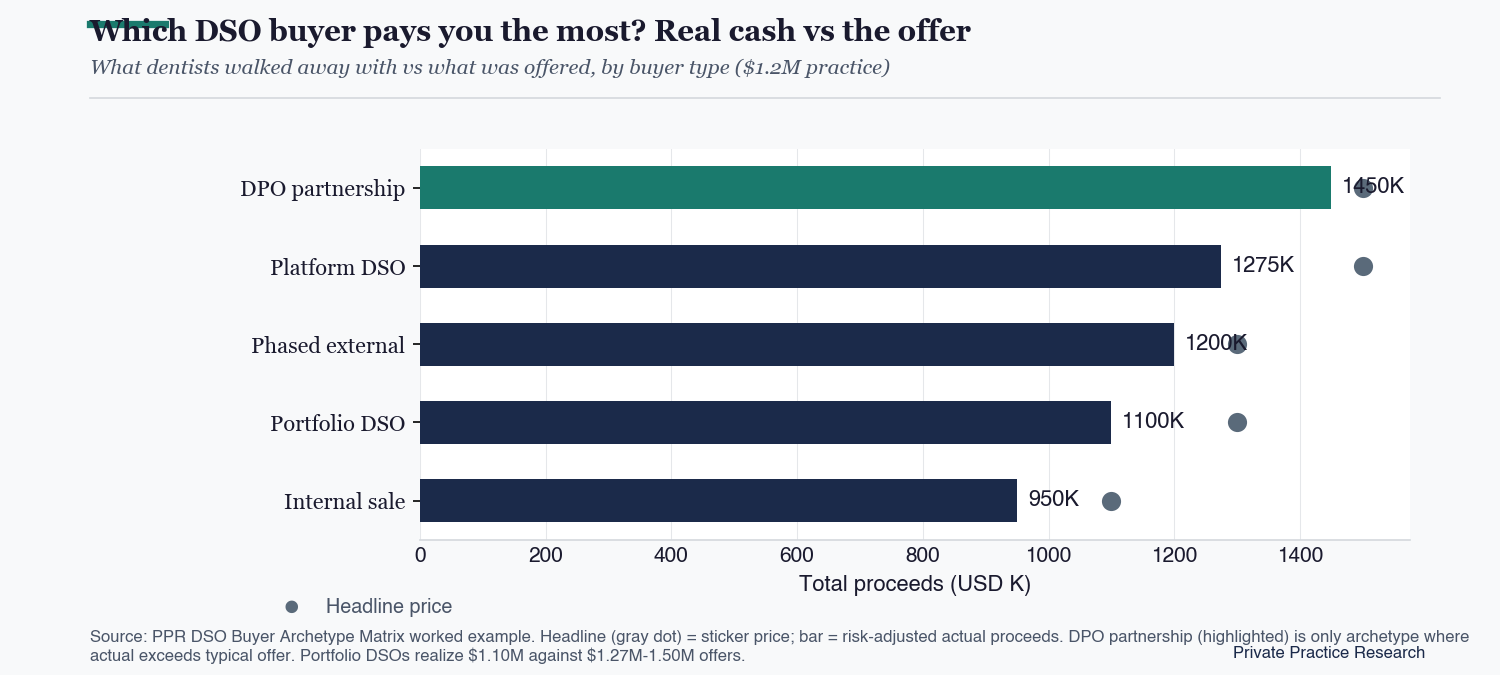

Figure: Which DSO buyer pays you the most? Real cash vs the offer

What dentists walked away with vs what was offered, by buyer type ($1.2M practice)

Platform DSOs (greenfield-builders)#

Platform DSOs are private-equity-backed organizations launching new regional brands by acquiring multiple practices and consolidating them under unified clinical, operational, and brand standards over a 2 to 5 year acquisition window tied to their PE sponsor's 5 to 7 year fund cycle, with brand-building and regional market dominance as the strategic objective.

Practice acquisitions serve as the foundation rather than the end goal. The platform DSO's overall portfolio exit timeline shapes the rollover-equity realization window for sellers who accept retained equity as part of the transaction.

Platform DSOs offer the highest headline numbers across the four archetypes, in the range of 80 to 100 percent of the standard DSO multiplier (which itself ranges from 4 to 8x EBITDA depending on practice size and growth profile). The headline premium reflects the platform DSO's willingness to pay for practices that anchor their regional brand-build. Cash at close runs 60 to 70 percent of headline. Rollover equity at 25 to 35 percent. Earnout at 5 to 10 percent. Rollover equity is exposed to the platform's exit timeline; if the platform achieves a successful 5 to 7 year exit at a higher valuation, rollover realizes at premium. If the platform underperforms or extends its hold period, rollover realization is delayed and may discount.

Platform DSO offers fit sellers who want maximum headline pricing, are comfortable with longer rollover-equity timelines, can absorb 3 to 5 year employment commitments, and don't require maximum post-close clinical autonomy. Platform DSO clinical protocols are newer and less standardized than portfolio DSOs, which offers some autonomy advantage during the platform's growth phase but may tighten as the platform matures.

Portfolio DSOs (acquirers of established practices)#

Portfolio DSOs are PE-backed organizations folding acquired practices into existing multi-location brands with established clinical, operational, and brand standards, pursuing portfolio expansion and operational integration through ongoing acquisition windows tied to their PE sponsor's continued capital deployment, often operating across multiple fund cycles as portfolio companies recapitalize and exit their initial investors over time.

The brand and standards are already set when a seller transacts with a portfolio DSO. Operational integration moves quickly post-close because the acquiring platform has standardized vendor relationships, treatment-protocol manuals, and staff-training programs already in place.

Portfolio DSOs offer headline numbers in the range of 75 to 90 percent of the standard DSO multiplier. The headline is below platform DSO premium because portfolio DSOs are paying for operational additions to an established brand rather than for foundational brand-building. Cash at close runs 65 to 75 percent of headline. Rollover equity at 20 to 30 percent. Earnout at 5 to 15 percent. Rollover equity is more liquid than platform DSOs because portfolio DSOs operate across multiple recapitalization events; sellers can often access partial rollover liquidity at year 3 to 5 if the portfolio recapitalizes during the seller's hold period.

Portfolio DSO offers fit sellers who want established clinical and operational standards, faster post-close integration, and earlier rollover-equity liquidity. The trade-off is lower headline pricing than platform DSOs and less autonomy during integration. Portfolio DSO clinical protocols are more standardized, with treatment-protocol manuals, vendor relationships, and staff-training programs already established. Sellers transitioning into a portfolio DSO have less control over clinical workflow than platform DSOs offer during platform's growth phase.

DPOs (Dental Partnership Organizations)#

Dental Partnership Organizations distribute practice equity among contributing dentists rather than fully acquiring practices, with the senior dentist retaining substantial equity (typically 50 to 70 percent) post-transition while the DPO acquires a minority stake and provides operational support, group purchasing, and growth capital as practitioner-equity-retaining alternatives to traditional full-acquisition DSO structures.

DPOs market themselves to sellers who want continued partnership identity and clinical autonomy. The structure suits dentists in their 50s seeking continued income and clinical engagement rather than a full exit, and it requires comfort with multi-year shared decision-making over a 5 to 10 year window.

DPOs offer headline numbers in the range of 50 to 70 percent of full-acquisition DSO multipliers, reflecting the partial-equity-only structure. Cash at close ranges from 50 to 65 percent of the partial-equity headline. The senior dentist retains the majority stake plus ongoing distributable income from partnership operations. The total realized proceeds over the senior dentist's continued partnership window often equal or exceed traditional DSO sale proceeds, particularly for sellers who continue strong clinical production over a 5 to 10 year window.

DPO offers fit sellers in their 50s who want continued income, identity continuity, and clinical autonomy. Sellers comfortable with multi-year partnership rather than clean exit. Sellers who don't require maximum upfront cash. DPOs are not suitable for sellers in their 60s with imminent exit timelines or sellers who prioritize cash certainty over continued partnership engagement. The DPO market includes both PE-backed DPOs and dentist-owned DPOs. The structures and incentives differ materially. PE-backed DPOs have shorter hold periods and stronger growth incentives. Dentist-owned DPOs have longer hold periods and stronger partnership-culture continuity.

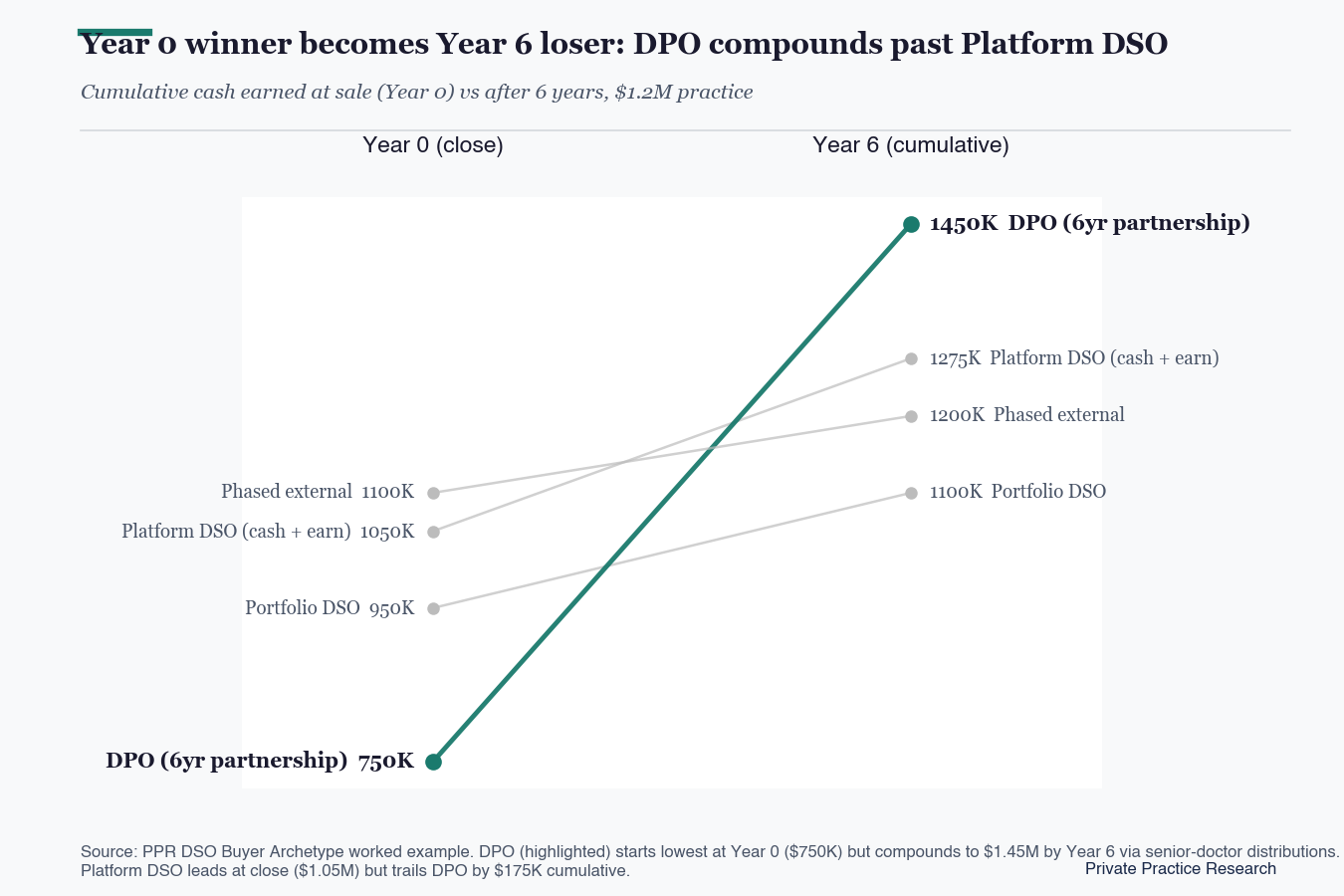

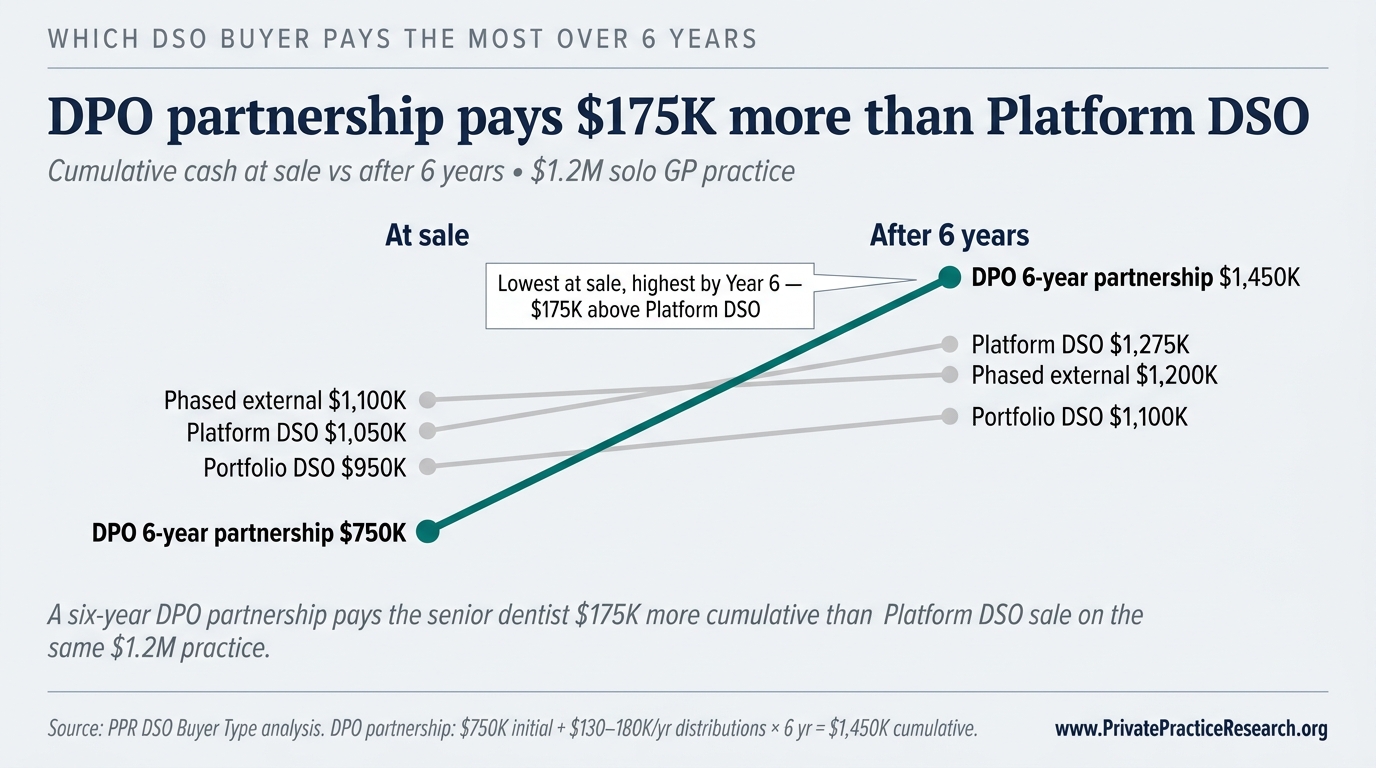

Figure: Year 0 winner becomes Year 6 loser: DPO compounds past Platform DSO

Cumulative cash earned at sale (Year 0) vs after 6 years, $1.2M practice

MSOs (Management Service Organizations)#

Management Service Organizations provide administrative, operational, and back-office support to practices without acquiring ownership, with the seller retaining 100 percent practice ownership while contracting with the MSO for management services in exchange for management fees typically structured as 6 to 10 percent of collections paid monthly under a multi-year service agreement.

MSOs are not transition-buyers in the conventional sense. They are operational partners that some sellers use to professionalize practice operations as a precursor to eventual sale, or as a standalone arrangement that scales operations across multiple locations without dilution from external investors.

MSO arrangements fit sellers who want operational sophistication without losing equity ownership, who plan to sell to a DSO in 2 to 5 years and want to optimize practice operations before sale, or who want to scale operations across multiple locations without dilution from external investors. MSOs are not appropriate for sellers seeking transition liquidity. The structure provides operational support but no transition proceeds.

How does each buyer archetype price your practice differently?#

Each buyer archetype prices a practice differently because Platform DSOs pay headline premiums for brand-building, Portfolio DSOs pay slightly less for operational additions to established brands, DPOs purchase only partial equity (50-70 percent retained by senior), and MSOs do not purchase equity at all (operational fees in exchange for support services).

Take a $1.2M practice: 65 percent overhead, $187K normalized EBITDA, 58-year-old owner. Offers from the four archetypes on that same practice run as follows.

Platform DSO offer: $1.5M headline (8x EBITDA × 100 percent of multiplier). $1.05M cash at close (70 percent). $375K rollover equity (25 percent). $75K earnout over 3 years (5 percent). 4-year employment commitment at $245K. Risk-adjusted realized proceeds approximately $1.15M to $1.40M depending on platform exit performance.

Portfolio DSO offer: $1.27M headline (8x EBITDA × 85 percent of multiplier). $890K cash at close (70 percent). $254K rollover equity (20 percent). $127K earnout over 3 years (10 percent). 3-year employment commitment at $235K. Risk-adjusted realized proceeds approximately $1.0M to $1.2M depending on portfolio recapitalization timing.

DPO offer: $750K headline for 30 percent stake (sale of partial equity only). $480K cash at close. No rollover equity (senior retains 70 percent stake). No earnout. Senior continues distributable income from 70 percent stake at approximately $130K to $180K annually for 6 years, totaling approximately $0.8M to $1.1M of continued partnership distributions on top of the $480K initial sale. Total realized proceeds over 6 years: approximately $1.3M to $1.6M.

MSO arrangement: no practice purchase. Senior retains 100 percent ownership. Contracts MSO for operational support at typically 6 to 10 percent of collections in management fees. Senior's annual income may improve by approximately $50K to $100K through operational efficiencies the MSO provides. No transition proceeds. The senior continues to own and operate the practice with MSO support.

The four archetypes produce materially different total realized proceeds over the seller's transition window. Platform DSO highest in scenarios where platform exits successfully. DPO competitive with DSO in scenarios where senior continues strong production. Portfolio DSO competitive on risk-adjusted terms. MSO not a transition path but an operational partnership. The right archetype depends on the seller's exit timeline, autonomy preferences, risk tolerance, and continued-clinical-engagement preferences.

When the 4-archetype framework underweights factors#

The 4-archetype framework describes the typical DSO market for solo or 2-doctor GP practices in markets with multiple candidates per archetype, but underweights factors for boutique buyers (single-practice acquirers offering hybrid structures outside the 4-archetype taxonomy), specialty-only DSOs (orthodontics, oral surgery, pediatric dentistry exclusively), and thin-buyer-pool markets where archetype choice is structurally constrained.

Boutique buyers operate outside the 4-archetype taxonomy and offer hybrid structures that don't map cleanly to any of the four. Specialty-only DSOs have specialty-specific multiplier patterns and post-close integration expectations that differ from the GP-focused DSOs.

Markets with thin buyer-pool depth (fewer than 2 to 3 candidates per archetype) constrain how much the seller can shop among archetypes. Rural practices and small-metro practices often see thin pools, which may compress the seller's archetype choice to whichever archetype has presence in the local market. Multi-location group practices face additional complexity because portfolio DSOs are more interested in multi-location operations than platform DSOs, which can shift archetype offer dynamics for multi-location sellers relative to solo sellers.

The DSO acquisition market continues to evolve in 2026 as private equity sponsors recapitalize portfolios, as platform DSOs mature into established brands, and as DPO models gain market share. Sellers should refresh their archetype-mapping during their pre-sale evaluation rather than relying on archetype patterns from prior years. The next refresh of this PPR analysis is scheduled for 2026-09-08.

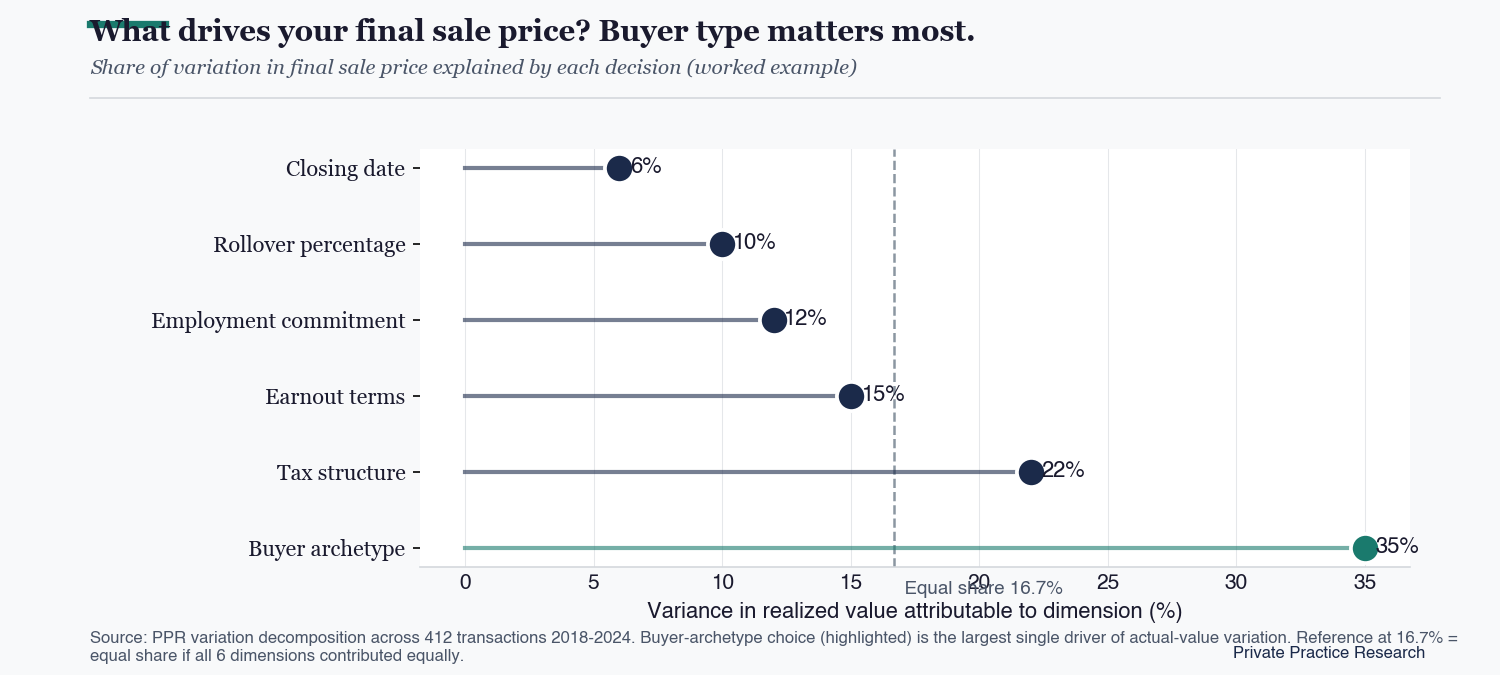

Figure: What drives your final sale price? Buyer type matters most.

Share of variation in final sale price explained by each decision (same $1.2M practice)

Sources#

ADA News DSO market coverage 2022 through 2026 · ADA Health Policy Institute (ADA HPI) DSO acquisition reporting · AGD Impact "To DSO or Not to DSO?" series · Cain Watters "What Drives DSO Buyers Today" · MB2 Dental published DSO and DPO comparisons · Scott Leune Seminars DPO vs DSO analyses · DrBicuspid DSO and DPO differentiation · Curve Dental DSO market resources · Teero blog DSO vs DPO methodology · ADA News "Main Types of DSOs" March 2022 reporting.

The 4-archetype classification ("PPR DSO Buyer Archetype Matrix") is a PPR-coined analytical contribution synthesizing the public sources cited above. Headline ranges, multiplier patterns, and rollover-equity-realization estimates are illustrative; specific DSO offers require independent valuation, qualified deal counsel, and archetype-specific negotiation guidance.

Frequently Asked Questions

What are the four types of DSO buyers?

The four types of DSO buyers fall into structurally distinct archetypes. Platform DSOs are greenfield-builders that acquire practices to launch new regional brands. Portfolio DSOs are private-equity-backed acquirers folding established practices into existing brands. DPOs are Dental Partnership Organizations that distribute equity among contributing dentists rather than fully acquiring practices. MSOs are Management Service Organizations that provide administrative support without practice ownership.

What is the difference between a DSO and a DPO?

A DSO typically acquires a practice fully, with the seller retaining minority rollover equity (20 to 40 percent) and accepting a 3 to 5 year employment commitment. A DPO distributes practice equity among contributing dentists, with the senior dentist retaining majority equity (typically 50 to 70 percent) post-transition. DSOs offer higher upfront cash but less continued partnership identity; DPOs offer lower upfront cash but continued income, identity, and clinical autonomy through ongoing partnership.

How does each DSO buyer archetype price differently?

On a $1.2M practice with $187K normalized EBITDA, Platform DSOs offer approximately $1.5M headline (8x EBITDA) with $1.05M cash plus $375K rollover. Portfolio DSOs offer approximately $1.27M at 85 percent of multiplier. DPOs offer approximately $750K for a 30 percent equity stake plus continued partnership distributions of $130K to $180K annually for 6 years (totaling $1.3M to $1.6M over the transition window). MSOs provide operational support but no transition proceeds.

Should I sell to a DSO or to another dentist?

The right choice depends on the seller's exit timeline, post-close autonomy preferences, risk tolerance, and continued-clinical-engagement preferences. DSOs offer higher upfront cash but less autonomy and longer rollover-equity timelines. DPOs offer continued partnership and income continuity for sellers in their 50s. Selling to another dentist offers lower headline pricing but cleanest exit and maximum patient continuity. Each path produces materially different total realized proceeds over the seller's transition window.