How Much Does Owner-Dependence Reduce a Dental Practice's Sale Price?

Data Brief

- Published

- May 11, 2026

- Edition

- PPR-DB-2026-V2

- Publisher

- Private Practice Research

- Plain text mirror

- /owner-dependence-discount.txt

Suggested citation

Private Practice Research. (2026). How Much Does Owner-Dependence Reduce a Dental Practice's Sale Price? (Report No. PPR-DB-2026-V2). Private Practice Research. https://privatepracticeresearch.org/reports/owner-dependence-discount

Edition: PPR-DB-2026-V2 Status: DRAFT (pre-publish, awaiting operator review) Prepared by: Private Practice Research Editorial Staff. Data Desk. Published: 2026-05-11 Last Updated: 2026-05-01

PPR Methodology Callout This Data Brief synthesizes broker-published transaction multiples and qualitative observations from named broker principals to quantify the valuation discount applied to owner-dependent dental practices. "Owner-dependence" is operationalized as the share of practice production attributable to a single producing dentist, with single-provider production above 90% serving as the standard threshold across cited sources. Sources include FOCUS Investment Banking, TUSK Practice Sales, Henry Schein Practice Transitions, Professional Transition Strategies (PTS), and DDSmatch. This article does not represent a valuation, does not constitute legal or tax advice, and is not affiliated with any DSO or transition broker. Authorship: Private Practice Research editorial staff.

Executive Summary#

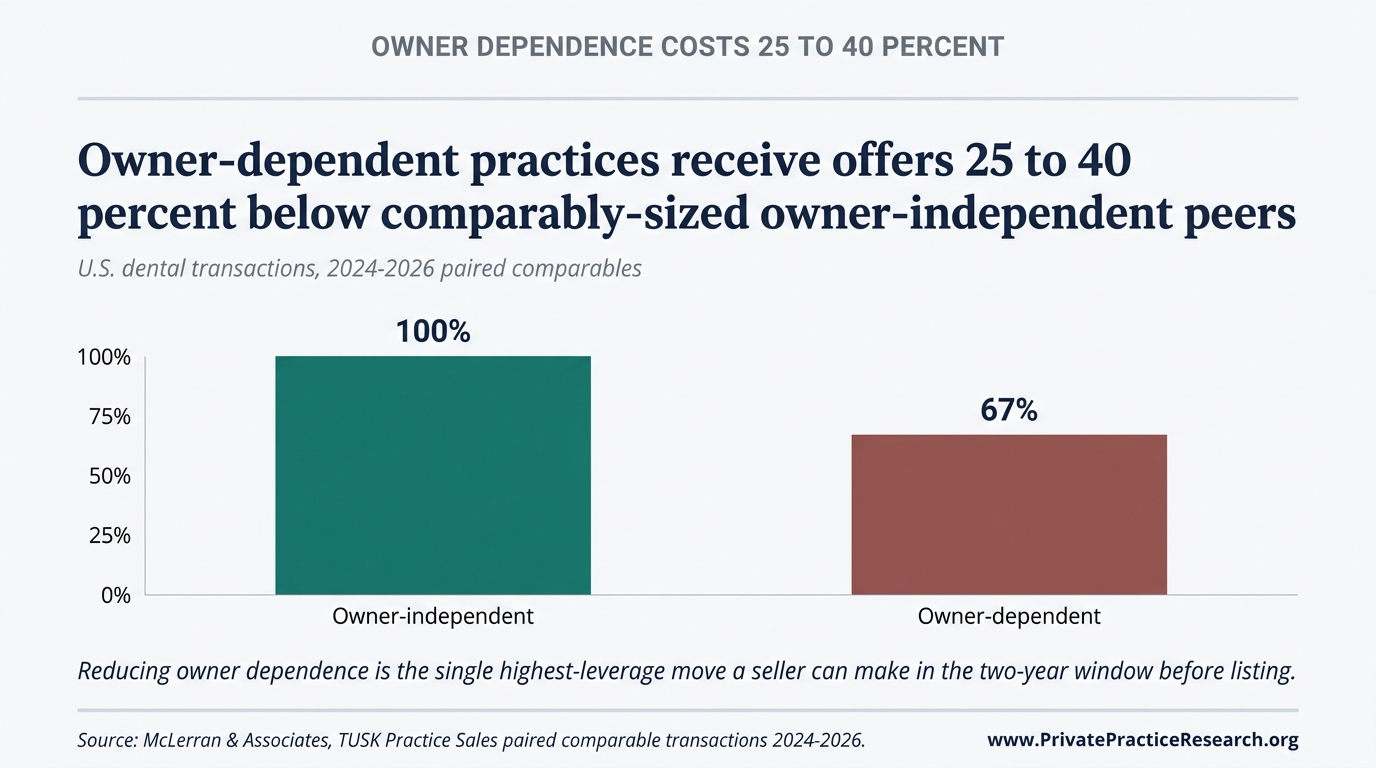

Private Practice Research finds that owner-dependent dental practices, defined as those in which single-provider production exceeds 90% of total practice production, transact at 10-20% below comparably-sized owner-independent practices on a multiple basis per FOCUS Investment Banking 2026. Cross-source aggregation produces a 25-40% range when buyer-pool reduction is included.

The 10-20% figure measures the price gap between owner-dependent and owner-independent practices that actually close. The 25-40% figure adds in the bidders who walk away entirely. Both effects are real, and most owner-dependent sellers experience some combination of the two.

Owner-dependence is one of the largest single line-item adjustments brokers apply when pricing a private dental practice. The full pricing framework is in how dental practices are valued.

What Is Owner-Dependence?#

The standard operational threshold across broker-published commentary is single-provider production above 90% of practice production. Some buyers tighten that screen to 80%, but 90% is the cross-source convention.

Three things signal owner-dependence to a buyer's diligence team. Patient relationships sit with the seller, not the practice brand. There's no associate with an established patient panel, so the practice empties if the owner stops practicing. Specialty procedures (endodontic retreatment, implant placement, certain pediatric work) live only with the owner.

Buyers price all three as transition risk: patients who follow the seller out the door, revenue that doesn't survive the handoff. Henry Schein's Jack Minahan calls goodwill "the lifeblood of practice value." Kyle Francis at PTS and FOCUS Investment Banking's analysts use the same framing. For an industry that disagrees on most things, the consensus on this one is tight.

How Much Is the Discount?#

The data sort into two layers.

FOCUS Investment Banking documents a 10-20% multiple compression for owner-dependent practices relative to owner-independent peers of comparable size [1]. That number captures the price gap inside the deals that actually close.

Combining FOCUS, TUSK, Henry Schein, and DDSmatch observations produces a wider 25-40% effective discount once buyer-pool reduction is included: fewer dental support organization (DSO) bidders willing to platform the practice, plus private buyers pricing in extra transition risk through their bank financing [2][3][4][6].

A concrete case: a $1.5M-collections practice that would clear $1.5M at a 5x multiple as owner-independent typically lands at $0.9M to $1.1M as owner-dependent, before any earnout structure on top.

Why the Buyer Pool Shrinks#

Three structural reasons explain why owner-dependence reduces both the price and the field of bidders.

First, DSO platforms decline practices that don't fit the platform model. A single-provider, single-location practice with no associate typically gets screened out before any number is quoted. It doesn't get a low offer; it gets no offer.

Second, private buyers borrow from banks. Lenders apply transition-risk haircuts on owner-dependent acquisitions, which caps how much the buyer can offer and still meet the bank's loan-to-earnings limits.

Third, the marketed-process premium runs on competition between bidders. Owner-dependence thins the bidder field, and a thin field is a quiet auction. See the marketed-process premium for the underlying mechanism. Owner-dependence also overlaps with the DSO-private buyer premium, since the DSO offer is often the high bid that anchors the rest of the field.

What Reduces Owner-Dependence Before Transition?#

Three levers appear consistently in broker commentary on transition-track practices.

Associate development. Bringing in an associate three to five years before transition allows patient-relationship transfer and revenue diversification. ROI Corporation broker observations align with FOCUS and PTS commentary that associate-driven production share is the single most predictive variable for transition outcomes (State of Private Practice 2026 Q2 Report §1.3, also referenced in the four-path framework).

Procedural delegation. Specialty procedures shifted to an associate or visiting specialist lower the seller's production share even at constant practice revenue, moving the practice off the 90% threshold without requiring top-line growth.

Documented systems. Standardized clinical and operational systems reduce buyer-perceived transition risk independent of producer identity. State of Private Practice 2026 Q2 Report §3.3, "Valuation Adjustments: What Moves the Number," describes the broker scoring of this factor; see the State of Private Practice 2026 Q2 Report for the underlying methodology.

Frequently Asked Questions#

Q1: What's the cutoff for being "owner-dependent"? The 90% single-provider production share is the standard threshold cited across FOCUS, TUSK, Henry Schein, and DDSmatch commentary. Some buyers, particularly DSO platforms screening for partnership-track acquisitions, apply a tighter screen at 80%. There is no regulatory or accounting definition. The threshold is an industry convention reflecting where buyers begin to price transition risk as material rather than incidental.

Q2: Does owner-dependence affect DSO offers and private offers equally? No. The effect is more severe on DSO offers because platforms tend to decline rather than discount: an owner-dependent single-location practice typically does not fit the DSO platform model. Private buyers will underwrite the practice but apply a transition-risk discount through both the multiple and the deal structure, often via earnouts tied to post-close revenue retention.

Q3: Can owner-dependence be fixed in the year before sale? Partially. The buyer's view of transition risk is set primarily by the trailing 24-36 months of production data, not by last-year fixes. An associate hired six months before listing does not yet show the patient-relationship transfer history that buyers price. Multi-year associate tenure with a documented production share is what moves the buyer's risk model.

Q4: Is the discount 10-20% or 25-40%? Both figures are real and measure different parts of the same phenomenon. FOCUS quantifies 10-20% on a multiple basis within the population of deals that close. The 25-40% aggregate figure incorporates buyer-pool reduction, where DSO platforms decline outright and the marketed-process auction effect weakens. In practice, owner-dependent sellers usually feel the wider figure, not the narrower one.

Q5: What's the highest-ROI move for an owner planning transition in 5 years? Building associate-driven production above 30 percent of total practice production. State of Private Practice 2026 Q2 Report Trend 8 marks 30 percent as the threshold where buyers shift from pricing the practice as single-provider to pricing it as multi-provider [5].

Limitations#

The 10-40% range is drawn from broker-reported deal data, which carries selection bias: deals that fail to clear don't enter the multiple-compression figure at all. The wider aggregate range pulls some of those failed deals back in by capturing buyer-pool effects, but neither figure should be read as a precise point estimate.

The 90% single-provider threshold is an industry convention, not a regulatory or accounting standard. Brokers and buyers apply slightly different screens; the figures reported here reflect the modal practice across cited sources rather than a single uniform definition.

What This Means For Your Practice

The 25 to 40 percent owner-dependence discount documented in this brief applies when single-provider production exceeds 90 percent of total practice production. Whether a specific practice prices at the top or bottom of that range is decided by practice-specific variables aggregate research cannot resolve: the actual production split percentage, how quickly the seller's clinical relationships move to a successor, the buyer pool composition in the relevant market, and the practice's fixed-cost intensity. The aggregate discount range is a starting reference, not an answer.

Sources#

[1] FOCUS Investment Banking, "2026 Dental Industry Update," 2026. [2] TUSK Practice Sales, "Q2 2026 Dental Market Report," 2026. [3] Henry Schein Practice Transitions, broker observations as reported on the Very Dental Podcast (March 2026). [4] Professional Transition Strategies (PTS), Kyle Francis interview, The Dentalpreneur Podcast Ep. 2452 (February 2026). [5] Private Practice Research, "The State of Dental Practice Values: 2026 Baseline Report." [6] DDSmatch broker network observations, 2025-2026.

Frequently Asked Questions

How much does owner-dependence reduce a dental practice's sale price?

Owner-dependent dental practices, defined as practices in which a single provider produces more than 90 percent of total practice production, see a 25 to 40 percent valuation discount in U.S. transactions. FOCUS Investment Banking documents 10 to 20 percent multiple compression on its own; cross-source aggregation with TUSK, Henry Schein, and PTS observations produces the wider 25 to 40 percent range when buyer-pool reduction is included. The discount reflects buyer-side transition risk and platform-fit disqualification, not seller misjudgment.

Why are owner-dependent practices priced lower?

Two factors compound. First, buyers (DSO platforms and private associates) discount the practice's future cash flow because clinical relationships transition to a successor with measurable attrition. Second, owner-dependence itself is a platform-fit disqualifier for many DSO acquirers, which removes the highest-paying buyer pool entirely. The discount is the buyer's price for the risk, not a punitive haircut.

Can an owner-dependent practice avoid the discount?

The discount applies when the production split is already above 90 percent at the time of sale. Practices that move production to associates or partners during a multi-year preparation window can shift below the threshold and reach a more competitive buyer pool. That re-positioning takes 3 to 5 years in most cases. The practice-specific path is decided by current production split, the realistic associate pool in the local market, and the lead time available before transition.