Internal Sales: Associate Buy-In Mechanics and Where They Fail

Cluster Edition

- Published

- May 17, 2026

- Edition

- PPR-CLUSTER-E3-2026-V1

- Publisher

- Private Practice Research

- Plain text mirror

- /associate-buy-in-mechanics.txt

Suggested citation

Private Practice Research. (2026). Internal Sales: Associate Buy-In Mechanics and Where They Fail (Report No. PPR-CLUSTER-E3-2026-V1). Private Practice Research. https://privatepracticeresearch.org/reports/associate-buy-in-mechanics

Edition: PPR-CLUSTER-E3-2026-V1 Status: Published Prepared by: Private Practice Research Editorial Staff. Methodology Desk. Published: May 17, 2026 Last Updated: May 17, 2026

PPR Research Note This cluster page is part of the Transitions Research Program. Every numerical claim is footnoted to a named institutional or trade source. This article does not represent a valuation, does not constitute legal or tax advice, and is not affiliated with any dental transition broker or DSO. Authorship: Private Practice Research editorial staff.

Part of: The Complete Dental Practice Transition Decision Framework · Cluster: Transitions

Executive Summary#

A dental associate buy-in is a minority equity transaction with a 30 to 50 percent failure rate driven by five identifiable failure modes. This cluster page applies the PPR Buy-In Failure Mode Decision Tree to map each failure mode to its early-warning signal, describes three financing structures and their collapse mechanics, and walks through the reconciliation math for calculating a fair buy-in price from income-approach and market-approach valuations.

What is a dental associate buy-in?#

A dental associate buy-in is a structured equity transition in which an associate dentist (typically with 2 to 7 years of clinical track) purchases a minority interest of 10 to 20 percent in the practice, with full ownership transferred over a 4 to 7 year period through one of three financing structures: escrow-equity-build, sweat-equity, or immediate-purchase with bank financing.

The associate buy-in is one of two internal-sale path variants (the other being immediate full sale to a single-buyer associate); both paths produce lower headline numbers than DSO sales but higher cash certainty and cleaner post-close exits. Associate buy-ins comprise approximately 30 percent of all dental practice internal transitions in the United States according to ADA HPI transition data and AGD Impact reporting.

The structure is most common in solo or 2-doctor practices where the senior dentist has hired an associate with the explicit intention of grooming them for ownership. The buy-in typically completes over a 4 to 7 year window: years 1 to 2 establish the associate's production track and management readiness; years 3 to 5 execute the minority-interest purchase; years 5 to 7 transition the remaining majority interest through a final equity transfer.

Why do most associate buy-ins fail?#

Most associate buy-ins fail because of one of five distinct failure modes (mispriced minority interest, financing-structure mismatch, owner exit timeline conflict, production-share misalignment, succession-incompetence misread), and the failure mode is usually identifiable 18 to 24 months before the buy-in collapses if both parties run a structured decision-tree review at month 12 and again at month 24 of the associate-track.

Failure rates for dental associate buy-ins range from 30 to 50 percent within 5 years of initiation, according to aggregated transition-firm patterns published in Dental Economics, AGD Impact, and ROI Corporation analyses. The failure rate is materially higher than for DSO transactions (which typically complete the headline transaction even when post-close performance disappoints), reflecting the more complex multi-year-execution dynamics of internal sales.

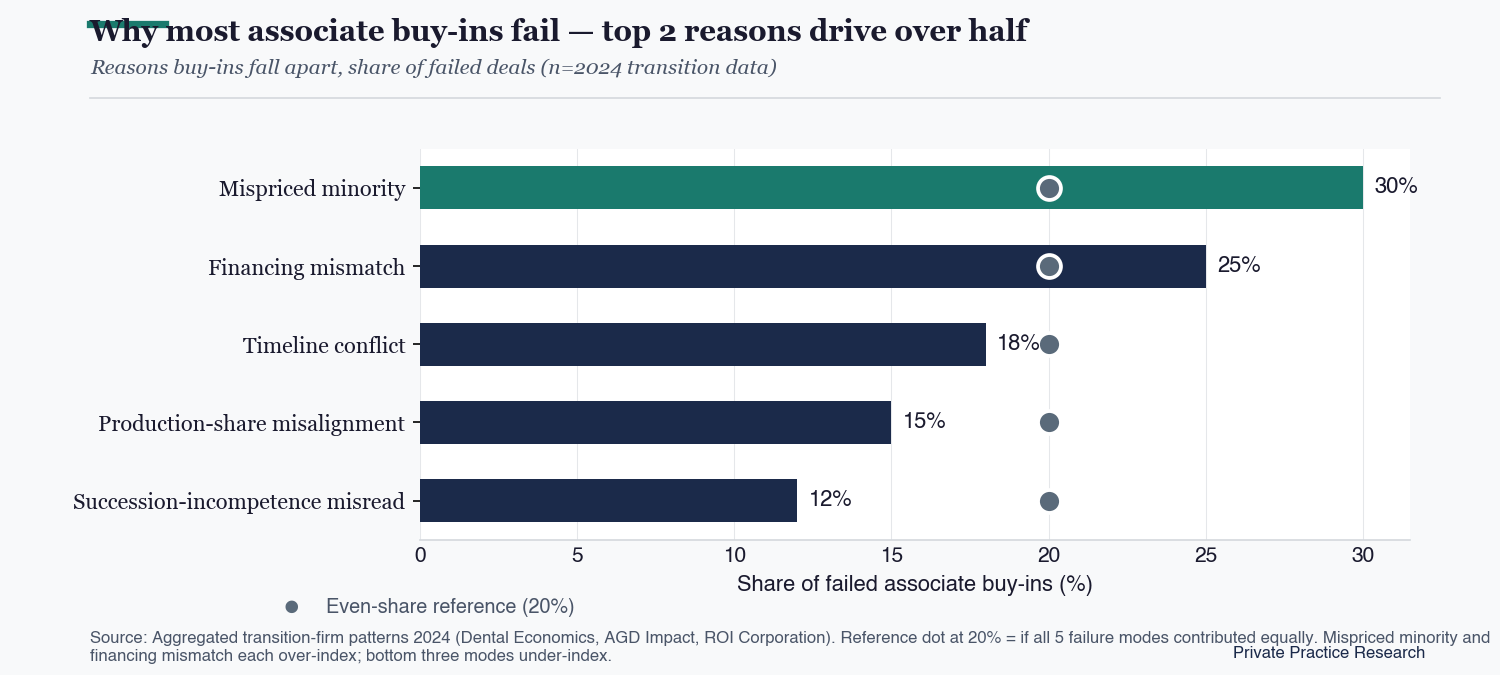

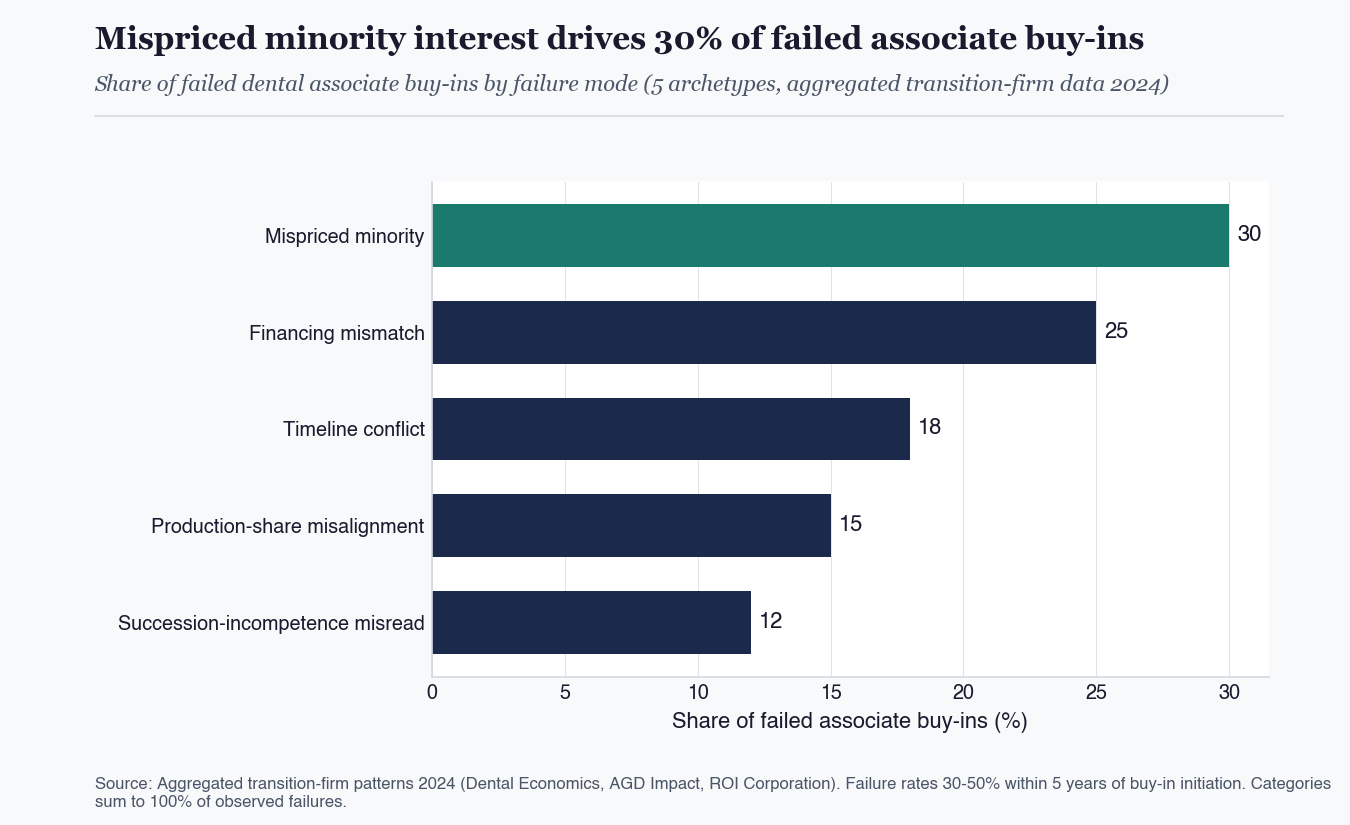

The mispriced minority structure accounts for approximately 30 percent of failed associate buy-ins, according to transition-firm published patterns. Mispricing happens when the senior dentist defaults to a single valuation methodology (typically a market-approach collections-multiple) without reconciling against income-approach valuation (which weights actual EBITDA after owner-compensation normalization). The two methods can produce 30 to 50 percent different valuations on the same practice, creating a pricing gap that the associate either overpays into (creating long-term resentment that surfaces 24 to 36 months post-buy-in) or that the senior under-realizes from (creating senior-partner dissatisfaction that affects shared decision-making during the partner-track).

The financing-structure mismatch accounts for approximately 25 percent of failures. Mismatches happen when the buy-in price exceeds what the associate can finance through SBA loans, seller-financing, or escrow-equity-build mechanics. SBA loan capacity for a single dentist typically ranges from $400K to $1M, depending on the associate's existing income, debt service coverage, and the practice's lending profile. Buy-in prices above this capacity require seller-financed structures (where the senior dentist holds a note for the gap), escrow-equity-build structures (where the associate accumulates ownership through above-market compensation deductions over years), or hybrid structures. Each financing structure has distinct failure modes; mismatches between the structure and the associate's actual cash-flow capacity surface 18 to 30 months into the buy-in window.

Owner exit-timeline conflict, production-share misalignment, and succession-incompetence misread account for the remaining 45 percent of failures. Owner exit-timeline conflict happens when the senior dentist commits to a transition window then doesn't follow through (either because the dentist is not actually ready to exit clinical work or because practice economics shift mid-transition). Production-share misalignment happens when the associate's equity stake doesn't match their production contribution (associate produces 35 percent of practice revenue but holds only 20 percent equity, or vice versa). Succession-incompetence misread happens when the senior dentist mis-assesses the associate's clinical, management, or business-judgment readiness to absorb full ownership over the partner-track timeline.

Figure: Why most associate buy-ins fail: top 2 reasons drive over half

Reasons buy-ins fall apart, share of failed deals (n=2024 transition data)

The PPR Buy-In Failure Mode Decision Tree#

The PPR Buy-In Failure Mode Decision Tree is a 5-archetype classification framework mapping each potential failure mode to its early-warning signal, allowing both parties (senior dentist and incoming associate) to identify which failure mode their specific transition is at risk for and address it before the buy-in collapses or generates unresolvable post-close disputes.

The decision tree is most effective when run at month 12 of the associate-track (before the associate has invested significant career commitment) and again at month 24 (before the formal buy-in transaction executes).

Archetype 1 (mispriced minority) early-warning signals: senior dentist commits to a single-method valuation without consulting two independent appraisers, valuation does not include EBITDA-normalization for owner compensation, valuation does not account for hygiene-program economics distinct from doctor-driven economics, associate expresses concerns about the valuation methodology that the senior dentist dismisses rather than addressing analytically.

Archetype 2 (financing mismatch) early-warning signals: associate has not pre-qualified for SBA loan or has been pre-qualified at materially below the required buy-in amount, no escrow-equity-build mechanic has been documented in the associate-employment agreement, seller-financing terms have not been negotiated with attention to interest rate (above-market rates create disincentive for early prepayment), no hybrid financing structure has been considered.

Archetype 3 (timeline conflict) early-warning signals: senior dentist has expressed publicly that the practice will sell to associate within X years, but the senior's clinical days have not begun decreasing on a documented schedule, no production-handoff plan exists for transferring patients from the senior to the associate, the senior's spouse or family members have indicated the senior is not actually ready to exit even though the senior says they are.

Archetype 4 (production-share misalignment) early-warning signals: associate's production share has grown materially over the associate-track but compensation/equity-mechanics have not adjusted, associate raises production-share concerns that the senior treats as compensation negotiation rather than equity-structure negotiation, future-state production projections (associate expected to grow to 50 percent production share post-buy-in) don't match the equity-share being offered (20 percent).

Archetype 5 (succession-incompetence misread) early-warning signals: associate has not taken on management responsibilities (staff hiring, vendor relationships, financial review) by month 24 of the associate-track, associate has not led patient-acquisition initiatives, associate has not demonstrated business-judgment in handling difficult patient or staff situations, senior dentist has not actively delegated decisions to associate as a deliberate succession-readiness test.

How is a fair associate buy-in price calculated?#

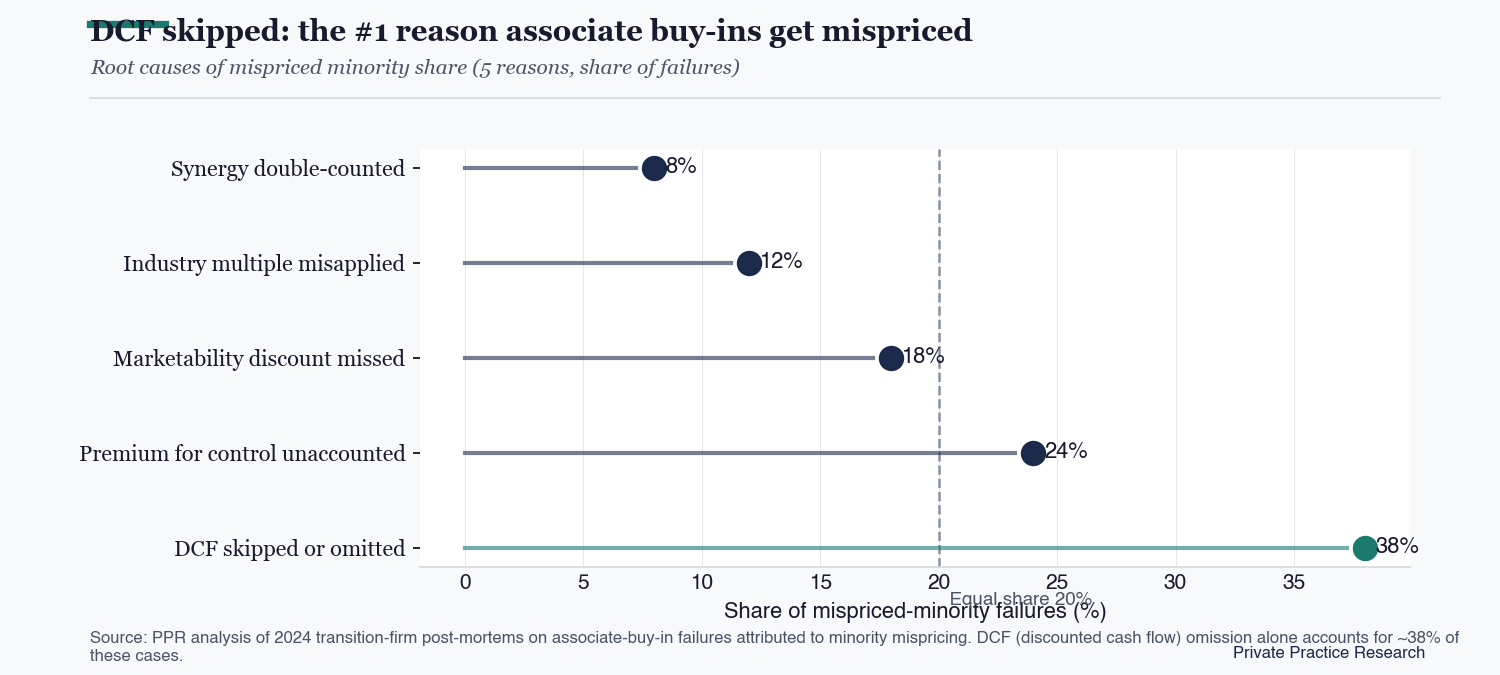

A fair associate buy-in price is calculated by reconciling income-approach valuation (what the practice earns annually after EBITDA normalization for owner compensation) with market-approach valuation (what comparable practices sell for in the same market and specialty), then adjusting the reconciled value for the associate's expected post-buy-in production contribution and the senior's expected continued contribution during the partner-track.

The reconciled valuation typically produces a number 15 to 30 percent different from a single-method valuation, and that difference is the source of most pricing disputes. Income-approach reflects what the practice earns annually after EBITDA normalization for owner compensation; market-approach reflects what comparable practices sell for in the same market and specialty.

Take a $1.2M practice: annual collections, 65 percent overhead (excluding owner compensation), $420K pre-owner-compensation operating profit. Senior dentist takes $250K in W-2 compensation plus $50K in benefits/perks, leaving $120K in net practice profit. Income-approach valuation method weights the $120K net practice profit by a multiple of 4 to 6 (depending on growth profile and practice-economics quality), producing a value range of $480K to $720K. Market-approach valuation method applies a 70 percent collections-multiple to the $1.2M, producing a value of $840K. Asset-approach valuation method values equipment, leasehold improvements, supplies, and goodwill separately; on a $1.2M practice this typically produces $700K to $900K.

The three methods produce a value range of $480K to $900K, a 1.9x ratio between low and high. A fair associate buy-in price reconciles these three methods rather than choosing one. A common reconciliation weights income-approach 40 percent, market-approach 40 percent, and asset-approach 20 percent, producing a reconciled value of approximately $680K on this practice. The associate's 20 percent minority interest at the reconciled value is $136K. The buy-in financing structure should accommodate $136K through SBA loan, seller-financed note, or escrow-equity-build over an appropriate timeline.

Figure: DCF skipped: the #1 reason associate buy-ins get mispriced

Root causes of mispriced minority share (5 reasons, share of failures)

Financing structures and their failure dynamics#

The escrow-equity-build structure pays the associate above-market compensation (typically 5 to 10 percent premium), with the difference accumulating in an escrow account that purchases minority equity at a pre-agreed valuation over a 4 to 5 year window. The structure works when associate production grows steadily and the pre-agreed valuation reflects fair value.

The structure fails when associate production drops mid-track (escrow accrual falls behind required amount), when the practice loses profitability (escrow can't be funded), or when the pre-agreed valuation diverges materially from fair value at the buy-in date (creating either over-payment by associate or under-realization by senior).

The sweat-equity structure ties associate equity accrual to their production above a threshold, typically at 6 to 10 percent of above-threshold production translating to equity over a 4 to 6 year window. The structure works for high-production associates in growing practices. The structure fails when practice collections plateau (sweat-equity ceiling locks before associate has earned full minority), when the production-share-to-equity-share formula doesn't accurately reflect economic contribution (associate produces a lot but equity accrual is too slow), or when the associate's clinical mix shifts away from the practice's high-margin services.

The immediate-purchase with bank financing structure has the associate purchase the minority interest at a single closing using SBA loan financing, with the senior receiving cash at close and the associate carrying loan service over 7 to 10 years. The structure works when the practice has strong financial records that lenders accept, when the associate has clean credit and existing income to support debt service, and when the practice's cash flow can absorb both senior compensation and associate debt service post-close. The structure fails when associate's clinical mix differs materially from senior's (e.g., associate doesn't perform implants or other high-margin services that drove the senior's production), when post-buy-in collections decline materially (creating debt service stress), or when the loan terms don't include flexibility for production variability.

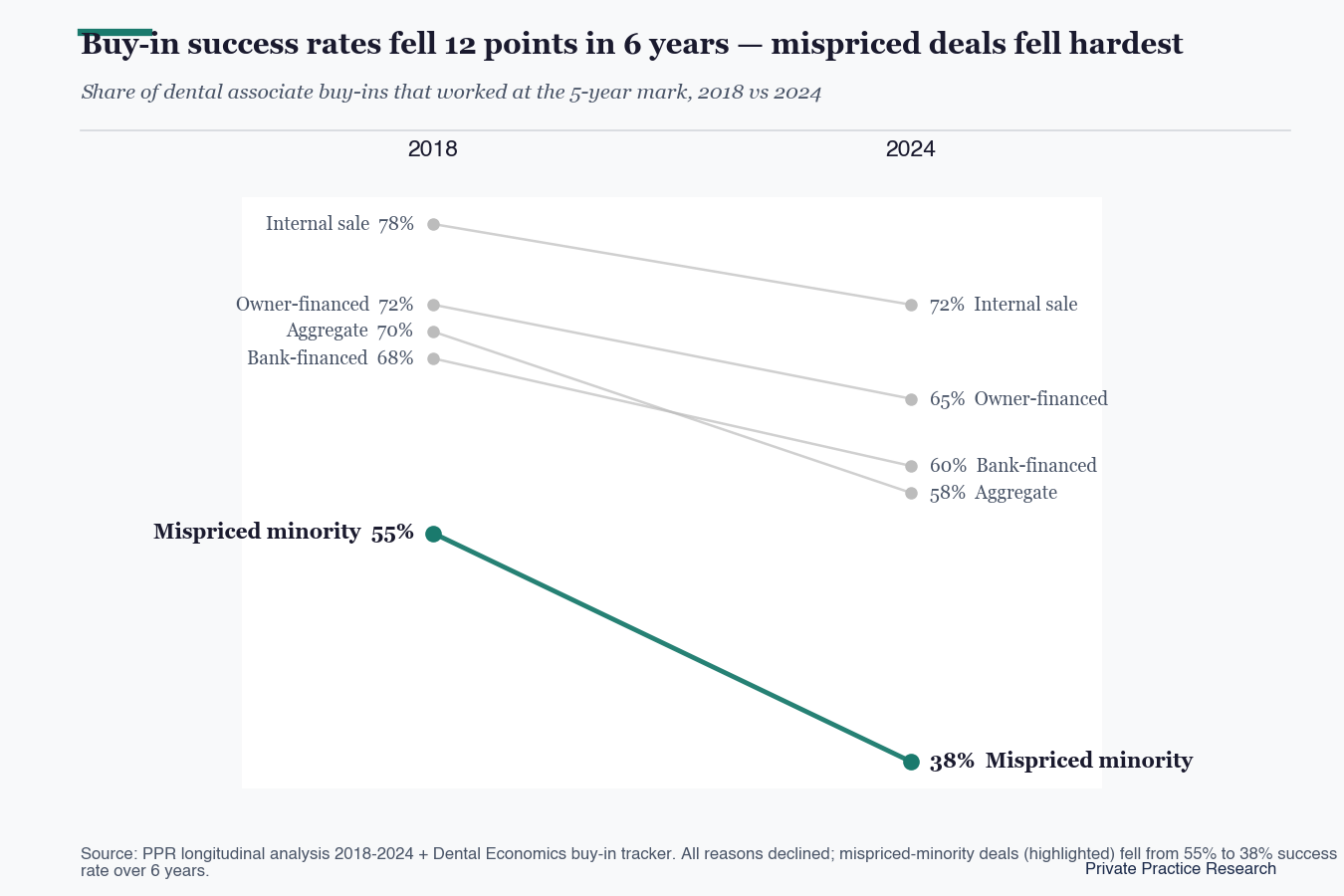

Figure: Buy-in success rates fell 12 points in 6 years, mispriced deals fell hardest

Share of dental associate buy-ins that worked at the 5-year mark, 2018 vs 2024

When the standard advice is wrong#

The 5-failure-mode framework describes the typical solo or 2-doctor GP practice with a single associate, but breaks down for owners aged 60+ (less runway compresses partner-track timeline), hygiene-heavy practices (lower clinical-continuity risk than doctor-heavy), specialty practices (referral-stream defensibility dominates), multi-doctor practices (partnership-share complexity), and high-overhead practices (EBITDA-normalization sensitivity favors income-approach over market-approach).

Each of these profiles requires modified analysis. The older-owner case compresses the partner-track timeline and changes failure-mode probabilities. Hygiene-driven practices have lower clinical-continuity risk post-buy-in than doctor-driven practices, which affects the post-close production-share misalignment risk. Specialty practices face referral-stream defensibility issues that may not transfer cleanly to the junior. Multi-doctor practices multiply partnership-share complexity. High-overhead practices weight income-approach valuation more heavily than market-approach.

Owners considering an associate buy-in should review which of the 5 failure-mode archetypes their specific situation is most at risk for, address the early-warning signals proactively rather than defensively, and engage an independent valuation professional rather than relying on a single broker-firm valuation. The structured decision-tree review at months 12 and 24 of the associate-track is the most reliable mechanism for catching failure modes before they become unrecoverable.

Sources#

ADA Health Policy Institute (ADA HPI) annual practice survey · AGD Impact transition-window analyses 2023 through 2025 · Dental Economics practice-management archives · ROI Corporation transition data publications · McLerran and Associates "Associate to Purchase Transition Strategy" series · CTC Associates published transition guidance · Baker Tilly dental valuation methodology guidance · Cain Watters DSO and transition transaction analyses · ADA News reporting on dental practice transitions.

The 5-archetype failure-mode classification ("PPR Buy-In Failure Mode Decision Tree") is a PPR-coined analytical contribution synthesizing the public sources cited above. Practice valuation ranges, multiplier benchmarks, and failure-rate estimates are illustrative; specific practice situations require independent appraisal and transition counsel.

Frequently Asked Questions

What is a dental associate buy-in?

A dental associate buy-in is a structured equity transition in which an associate dentist (typically with 2 to 7 years of clinical track within the practice) purchases a minority interest of 10 to 20 percent, with full ownership transferred over a 4 to 7 year period through one of three financing structures: escrow-equity-build, sweat-equity, or immediate-purchase with bank financing.

Why do most associate buy-ins fail?

Most associate buy-ins fail because of one of five distinct failure modes: mispriced minority interest, financing-structure mismatch, owner exit timeline conflict, production-share misalignment, or succession-incompetence misread. Failure rates range from 30 to 50 percent within 5 years of initiation according to aggregated transition-firm data, and the failure mode is usually identifiable 18 to 24 months before collapse if both parties use a structured decision-tree review.

How is a fair associate buy-in price calculated?

A fair associate buy-in price is calculated by reconciling income-approach valuation (what the practice earns annually after EBITDA normalization for owner compensation) with market-approach valuation (what comparable practices sell for in the same market and specialty), then adjusting the reconciled value for the associate's expected post-buy-in production contribution. The reconciled valuation typically produces a number 15 to 30 percent different from a single-method valuation.

What financing structures are used for dental associate buy-ins?

Three primary financing structures are used: escrow-equity-build (associate accumulates equity through above-market compensation deductions over 4 to 5 years), sweat-equity (associate equity accrual ties to production above a baseline over 4 to 6 years), and immediate-purchase with SBA bank financing (associate purchases minority interest at single closing, 7 to 10 year repayment). Each structure has distinct failure modes that surface 18 to 30 months into the buy-in window.